Bimetallism is a monetary standard in which the value of the monetary unit is defined as equivalent to certain quantities of two metals, typically gold and silver, creating a fixed rate of exchange between them.

There was much debate in the run-up to the election over how to define the rate between gold and silver in the US. Here’s where The Wizard of Oz comes in:

Dorothy is whipped out of Kansas by a tornado with her little dog “Toto” (short for teetotalers, who made a loud noise yip-yapping but were otherwise ineffective political companions). On her way to the Land of Oz, Dorothy picks up her electoral coalition. First, the Scarecrow, representing western farmers. “He thinks that he has no brains because his head is stuffed with straw. But we soon learn that he is shrewd and capable. He brings to life a major theme of the free silver movement: that the people, the farmer in particular, were capable of understanding the complex theories that underlay the choice of a standard.”

Next, the Tin Man (or Tin Woodman). The working class man, once a true human, is now just a cog in the industrial machine. Piece by piece his human body was replaced by metallic parts. He is now little more than a machine, a heartless (literally) machine. The Populist hope of the era was a grand farmer-labor coalition that never quite solidified — and we still see residual evidence of this hope in the official name of Minnesota’s Democratic Party, the Democratic-Farmer-Labor Party.

The Cowardly Lion, then, was William Jennings Bryan himself. Capable of a great roar — his speeches were legendary — alas, to mix metaphors, he was all bark and no bite.

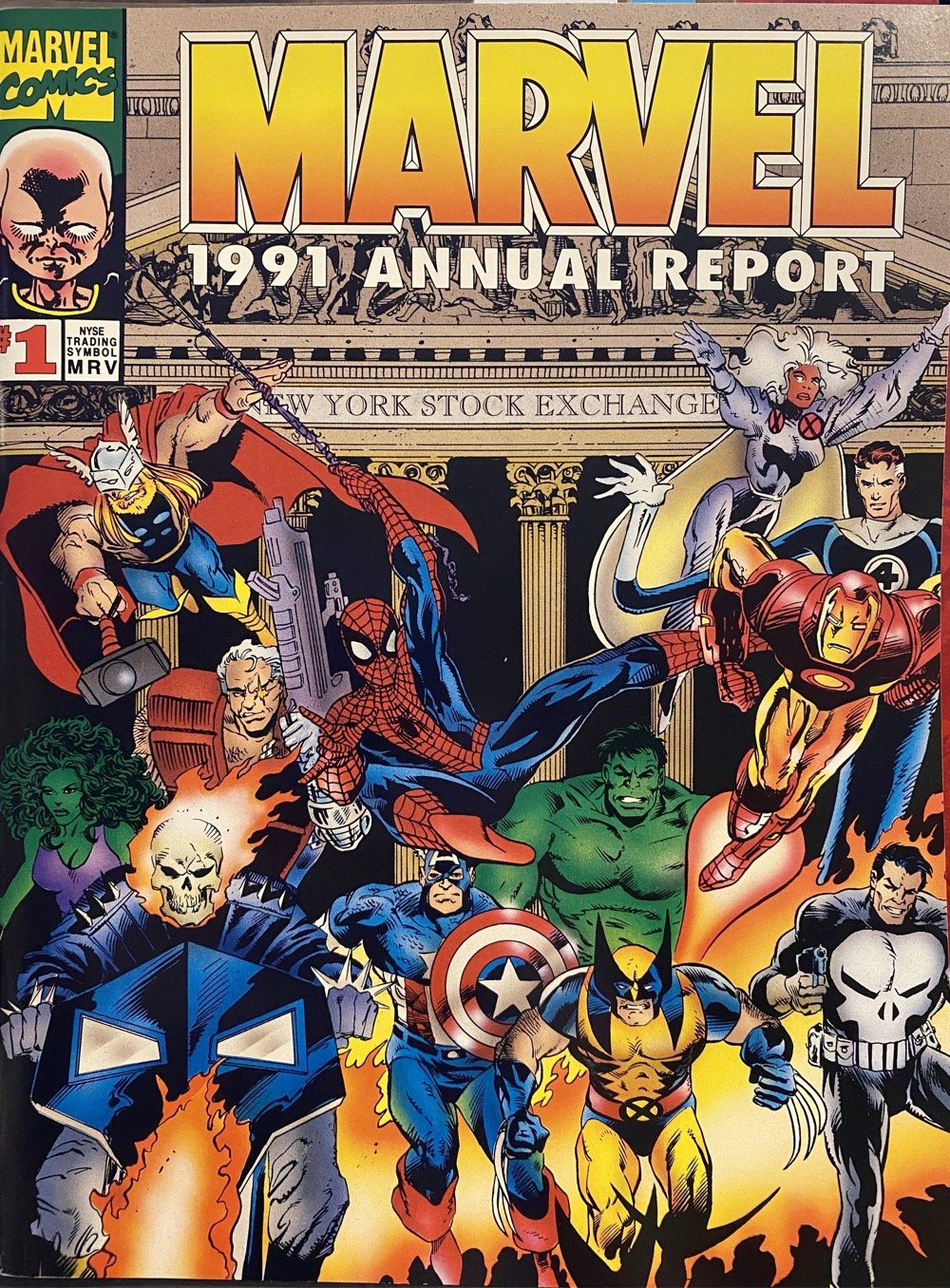

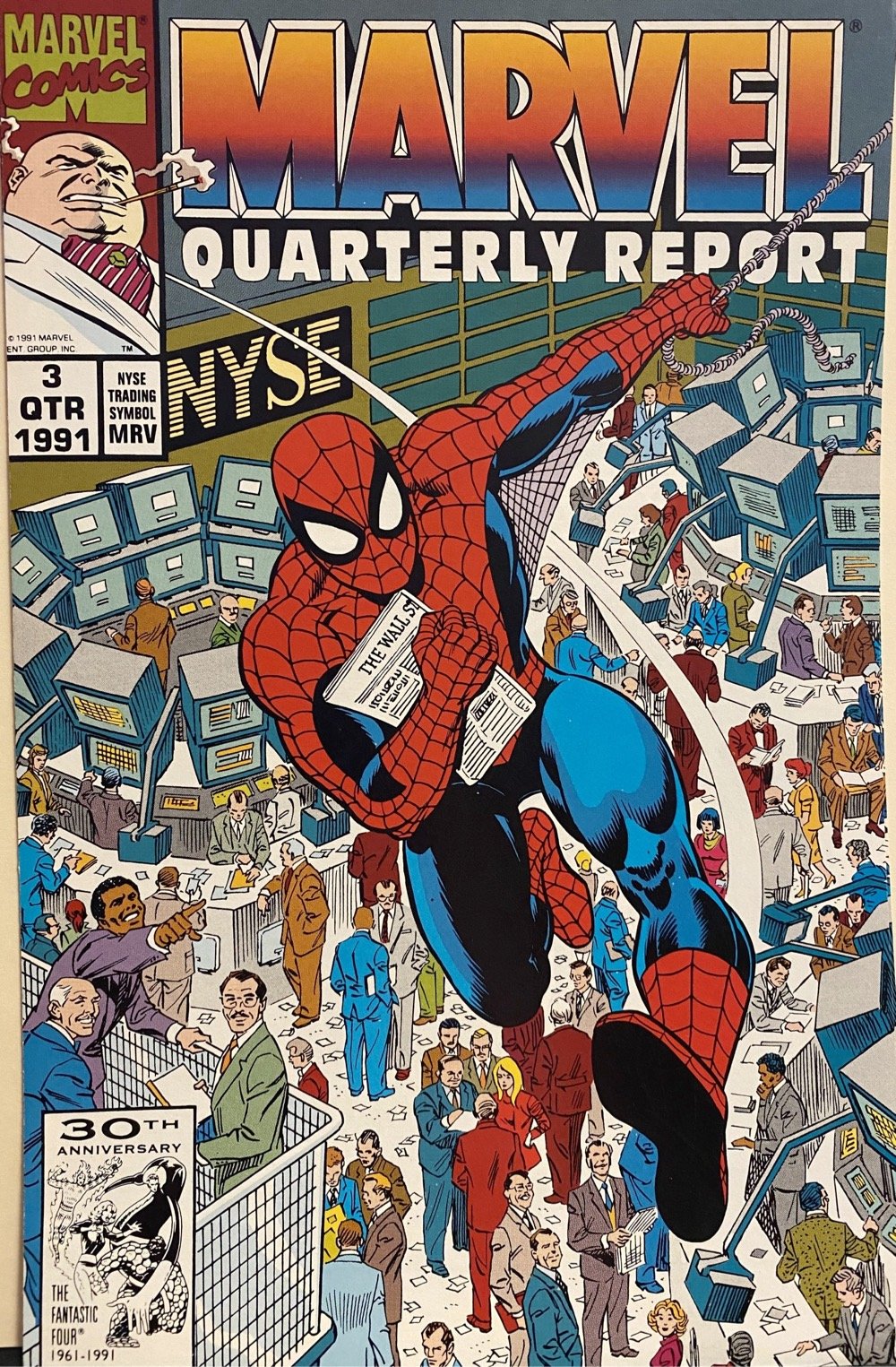

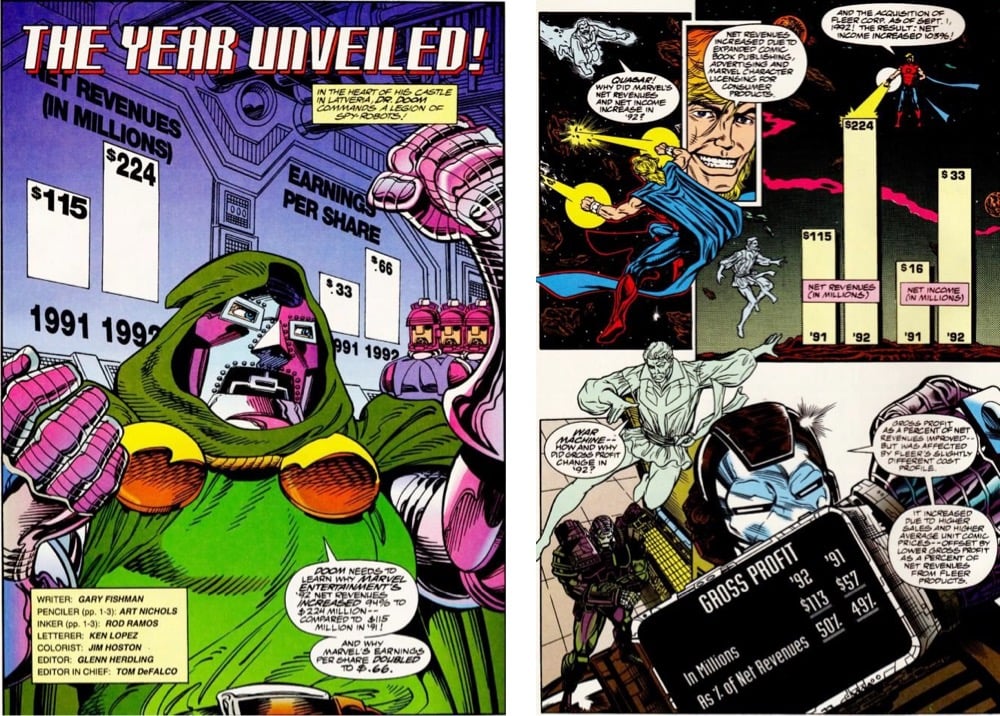

Starting in 1991 and continuing through 1996, Marvel released their quarterly and annual financial reports to shareholders in the form of comic books. Columbia University librarian Karen Green writes:

Working with editor Glenn Herdling, and using the Marvel Method of story to art to dialogue, Fishman developed the plot, Herdling found some of Marvel’s best artists to pencil, ink, and color, then Fishman wrote the copy (conveying everything the lawyers and SEC demanded), and Herdling put everything together. And so, thirty years ago today, a slim four-page comic debuted, with a cover by legendary artist John Romita Sr. Inside, Spider-Man and the Incredible Hulk (sporting, appropriately, an accountant’s green eye shade) discussed net income, publishing revenues, and earnings per share.

The report caused an immediate sensation. No one had seen anything like it. Even more impressive was the subsequent annual report. A 36-page stapled book on glossy paper, it combined information in comics form, introduced by Uatu the Watcher, with updates on licensing, advertising, and more, along with traditional financial tables and text.

The Western response has been far broader than most experts anticipated, and threatens to throw the Russian economy into chaos. Yet there’s a catch. Absent significant domestic reforms in the West — reforms that should have been enacted long ago — sanctions targeted at the oligarchic and official figures close to Russian President Vladmir Putin risk inflicting little more than a flesh wound on Russia’s imperial kleptocracy.

Rampant financial anonymity in places like the U.S. makes it relatively easy for powerful rich people to evade sanctions. A Russian oligarch may have multimillion-dollar mansions in Washington, D.C.; or multiple steel plants across the Rust Belt; or a controlling stake in a hedge fund in Greenwich, Connecticut; or an entire fleet of private jets in California; or an array of lawyers setting up purchases at art houses around the country. And all of that wealth can be hidden-perfectly legally-behind anonymous shell companies and trusts that are enormously difficult to penetrate.

If Western policy makers hope to hold Putin’s cronies truly accountable, sanctions will have to be paired with pro-transparency reforms that can disassemble this web of secrecy. Western governments should start by ending anonymity in shell companies and trusts; demanding basic anti-money-laundering checks for lawyers, art gallerists, and auction-house managers; and closing loopholes that allow anonymity in the real-estate, private-equity, and hedge-fund industries. That is, if the sanctions are to retain their bite, the entire counter-kleptocracy playbook needs to be implemented-immediately.

In this entertaining and informative video, Oliver Bullough, who has written a pair of books on money laundering (Moneyland and the forthcoming Butler to the World) takes us on a tour of London while telling us how “the most efficient scaled-up money laundering system in the world” has helped Russia’s oligarchs hide their billions and keep Putin in power. Bullough also wrote about the UK’s role in laundering oligarch money recently in The Guardian.

Russia is a mafia state, and its elite exists to enrich itself. Democracy is an existential threat to that theft, which is why Putin has crushed it at home and seeks to undermine it abroad. For decades, London has been the most important place not only for Russia’s criminal elite to launder its money, but also for it to stash its wealth. We have been the Kremlin’s bankers, and provided its elite with the financial skills it lacks. Its kleptocracy could not exist without our assistance. The best time to do something about this was 30 years ago — but the second best time is right now.

We journalists have long been writing about this, but it is not simply overheated rhetoric from overexcited hacks. Parliament’s intelligence and security committee wrote two years ago that our investigative agencies are underfunded, our economy is awash with dirty money, and oligarchs have bought influence at the very top of our society.

Americans are collectively almost $15 trillion in debt, most of it related to housing (i.e. mortgage debt). For the New Yorker, Margaret Talbot shares some images from Brittany Powell’s The Debt Project, a series of 99 portraits of Americans in debt.

Powell set about photographing ninety-nine Americans who owe money (she ended up with a few more, including herself, but started with that figure as a reference to the slogan “We are the ninety-nine per cent”) and asked them to handwrite accompanying text about how much they owe, and to whom. The litany of reasons gets repetitive, because that’s how it goes — difficulty finding a job in one’s field after graduating during the recession, a bad marriage, a bad divorce, vertiginous rents in expensive cities, medical crises, many, many student loans. Occasionally, there are epic and awful variations: one woman’s mother took out credit cards in her name and, in a ten-year period, racked up “a mortgage worth of debt” to fund her “compulsive shopping and hoarding habits.”

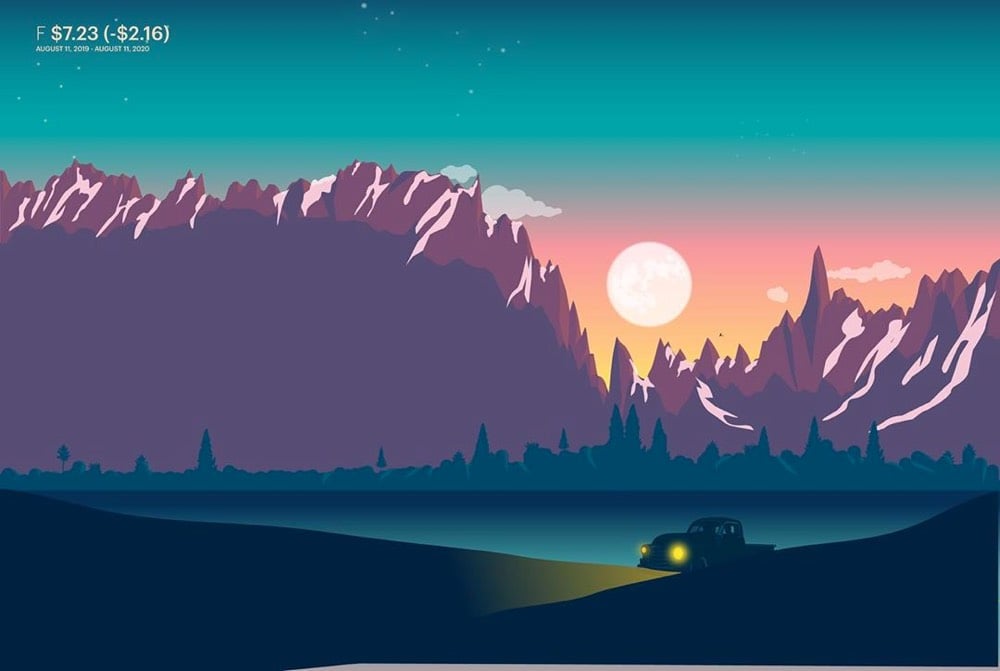

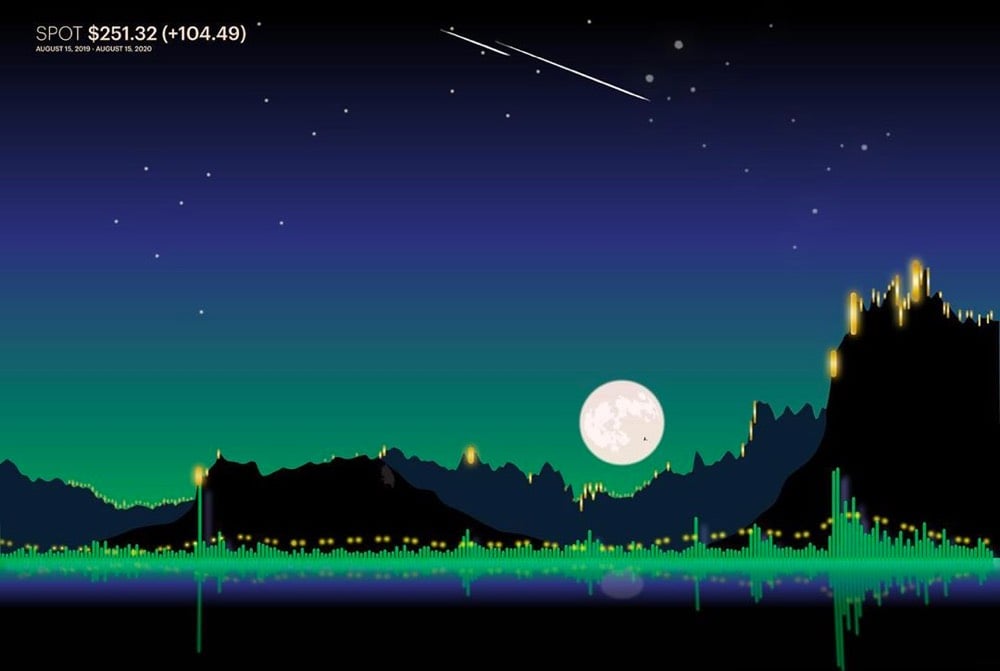

Inspired by the charts on Robinhood and Yahoo Finance, Gladys Orteza is turning the charts of notable stocks into landscape artworks, inserting references to the company into the art. The Ford chart at the top has a truck, the Tesla chart features a rocket (a reference to SpaceX), and the Disney one includes the twin suns of Tatooine & a Jawa Sandcrawler.

For Slate’s 2015 podcast series The History of American Slavery, Andrew Kahn created an interactive visualization of the 20,000+ voyages that made up the Atlantic slave trade that lasted 315 years. A video of the interactive map is embedded above.

As we discussed in Episode 2 of Slate’s History of American Slavery Academy, relative to the entire slave trade, North America was a bit player. From the trade’s beginning in the 16th century to its conclusion in the 19th, slave merchants brought the vast majority of enslaved Africans to two places: the Caribbean and Brazil. Of the more than 10 million enslaved Africans to eventually reach the Western Hemisphere, just 388,747 — less than 4 percent of the total — came to North America. This was dwarfed by the 1.3 million brought to Spanish Central America, the 4 million brought to British, French, Dutch, and Danish holdings in the Caribbean, and the 4.8 million brought to Brazil.

Roughly 400,000 enslaved Africans were brought to the United States before the practice was banned in 1808. The ban was mostly (but not entirely) enforced and yet in 1860, the population of enslaved persons was almost 4 million in the South. That’s because the 1808 ban, according to Ned & Constance Sublette’s book The American Slave Coast: A History of the Slave-Breeding Industry, was a form of trade protectionism that protected the forced breeding of enslaved peoples by American slaveowners. From a review of the book:

In fact, most American slaves were not kidnapped on another continent. Though over 12.7 million Africans were forced onto ships to the Western hemisphere, estimates only have 400,000-500,000 landing in present-day America. How then to account for the four million black slaves who were tilling fields in 1860? “The South,” the Sublettes write, “did not only produce tobacco, rice, sugar, and cotton as commodities for sale; it produced people.” Slavers called slave-breeding “natural increase,” but there was nothing natural about producing slaves; it took scientific management. Thomas Jefferson bragged to George Washington that the birth of black children was increasing Virginia’s capital stock by four percent annually.

Here is how the American slave-breeding industry worked, according to the Sublettes: Some states (most importantly Virginia) produced slaves as their main domestic crop. The price of slaves was anchored by industry in other states that consumed slaves in the production of rice and sugar, and constant territorial expansion. As long as the slave power continued to grow, breeders could literally bank on future demand and increasing prices. That made slaves not just a commodity, but the closest thing to money that white breeders had. It’s hard to quantify just how valuable people were as commodities, but the Sublettes try to convey it: By a conservative estimate, in 1860 the total value of American slaves was $4 billion, far more than the gold and silver then circulating nationally ($228.3 million, “most of it in the North,” the authors add), total currency ($435.4 million), and even the value of the South’s total farmland ($1.92 billion). Slaves were, to slavers, worth more than everything else they could imagine combined.

You can read more about the economics of slavery in this post from 2016, including how American banks sold bonds that used enslaved persons as collateral to international investors. (via open culture)

Last week, the beloved NYC eating establishment City Bakery closed its doors due to financial troubles.1 Rachel Holliday Smith dug into what happened for The City. It sounds like the company over-expanded, couldn’t get out of the debt it took on, and got into a series of increasingly bad lending situations.

One of those bad deals was borrowing $75,000 from a financial services firm called Kalamata Capital Group and promising to pay back $105,000. That’s a 40% interest rate, firmly in loan shark territory. But this is the bit that really got my eyebrows heading north (especially the bit in italics):

In a statement, the chief operating officer of Kalamata Capital Group, Brandon Laks, said the company “is truly sorry City Bakery decided to close” and stressed that many Kalamata Capital Group employees loved the establishment.

He said KCG made amendments to the funding agreement as City Bakery struggled and “without KCG’s capital and amendments, City Bakery would have closed, and jobs would have been lost, much sooner.”

“Unfortunately, many small businesses close and it is a risk KCG takes when we help fund and support these businesses,” he said.

Let’s be clear here: City Bakery was primarily a place for folks who can afford $5 croissants, but this is one of those instances where capitalism has become deeply disconnected from the people it’s allegedly supposed to benefit. All those KCG employees that loved City Bakery? Meaningless bullshit. A local lender that wants to invest in the community and its businesses doesn’t charge 40% interest. City Bakery needed some solid financial advice, a plan for getting out from under their debt (if possible), and a loan with decent terms. All KCG did was give City Bakery more rope to hang themselves and called it “support”.

Update: A couple people have pointed out that we don’t know the length of the loan and so cannot calculate the annual interest rate. Even so, as the article details, these “merchant cash advance” loans are under increasing scrutiny for being predatory:

As the Duncans soon learned, tens of thousands of contractors, florists, and other small-business owners nationwide were being chewed up by the same legal process. Behind it all was a group of financiers who lend money at interest rates higher than those once demanded by Mafia loan sharks. Rather than breaking legs, these lenders have co-opted New York’s court system and turned it into a high-speed debt-collection machine. Government officials enable the whole scheme. A few are even getting rich doing it.

I was in NYC last week and City Bakery shuttered on the very day I was going to wander over for one of their chocolate chip cookies, my #1 all-time favorite cookie.↩

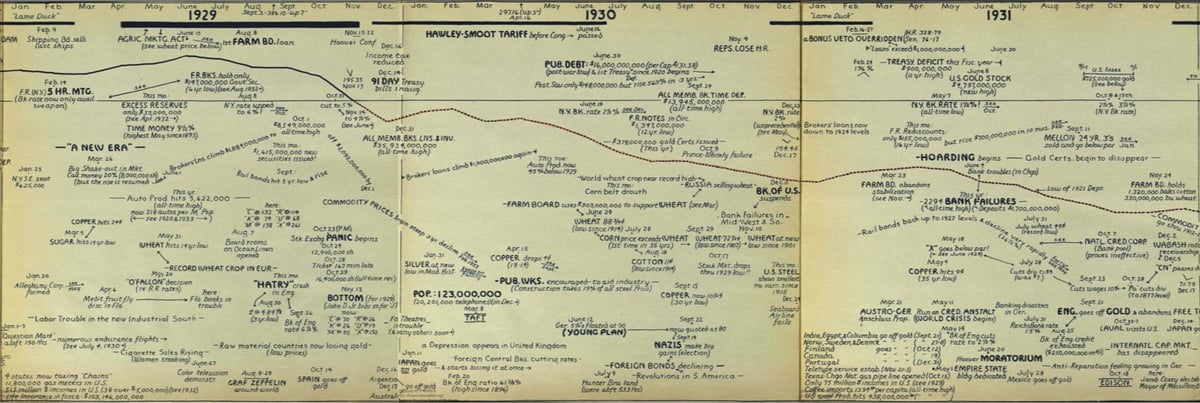

In 1936, former director of research at the Cleveland Federal Reserve L. Merle Hostetler published 75 Yrs. of American Finance, a hand-drawn chart of the economic health of the US from 1861 to 1935. The chart, which is horizontally oriented, shows a trending business activity index (which measures productivity) along with other financial data, indicates when Congress is in session, lists notable news events, and shows the high and low of the DJIA (starting in 1898). The graphic at the top shows Hostetler’s chart from 1929-1931, aka the beginning of the Great Depression.

The copy of this chart hosted by the St. Louis Fed goes to 1938…it must have been updated at some point. Also, if you go into the “»” menu in the upper-right corner of the in-page document viewer, you can set it to “horizontal scrolling” for easier viewing. (thx, andy)

Dollar Street is a project by Anna Rosling Rönnlund that imagines the world as a street ordered by income…poor families live at one end and rich families live at the other. A team of photographers went out and photographed the everyday items owned by families of all income levels — shoes, toothbrushes, TVs, beds, lights, sinks — so that visitors to the site can see how much income affects how families live.

Everyone needs to eat, sleep and pee. We all have the same needs, but we can afford different solutions. Select from 100 topics. The everyday life looks surprisingly similar for people on the same income level across cultures and continents.

Rönnlund explained her project at TED recently:

Bill Gates, who lives just one house in from the very end of the street (Bezos currently occupies the cul de sac), wrote about Dollar Street recently:

Income can often tell you more about how people live than location can. Whenever I visit a new place, I look for clues about which income level local families live on. Are there power lines? What kind of roofs do the houses have? Are people riding bikes or walking from place to place?

The answers to these questions tell me a lot about the people there. If I see power lines, I know homes probably have electricity in this area — which means that kids have enough light to do their homework after the sun sets. If I see patchwork roofs, families likely sleep less during the rainy season because they’re wet and cold. If I see bikes, that tells me people don’t have to spend hours walking to get water every day.

However, Gates’ conclusion — “It’s a beautiful reminder that we have more in common with people on the other side of the world than we think” — is not what I would take away from this. (via @roeeb/status/994474179339501568)

Using Beanie Babies, Chicken McNuggets, and the comedy talents of Keegan-Michael Key, John Oliver tries to explain the wild world of Bitcoin, blockchain, and cryptocurrency, the latter of which he describes as “everything you don’t understand about money combined with everything you don’t understand about computers”.

My favorite part was the explanation of how difficult hacking the blockchain is: “[like] turning a Chicken McNugget back into a chicken”.

This was very hard to keep watching after Oliver started detailing cryptocurrency scams and charlatans trying to take advantage of people. One of Oliver’s targets, Brock Pierce, was actually canned from the company he co-founded after the segment aired.

Ten years ago, investor Warren Buffett made a bet with Ted Seides of the investment firm Protégé Partners about the relative performance of index funds and hedge funds. The bet stated:

Over a ten-year period commencing on January 1, 2008, and ending on December 31, 2017, the S&P 500 will outperform a portfolio of funds of hedge funds, when performance is measured on a basis net of fees, costs and expenses.

Buffett has long been critical of money managers, recommending that most people put their money into low-fee index funds instead.

Over the years, I’ve often been asked for investment advice, and in the process of answering I’ve learned a good deal about human behavior. My regular recommendation has been a low-cost S&P 500 index fund. To their credit, my friends who possess only modest means have usually followed my suggestion.

I believe, however, that none of the mega-rich individuals, institutions or pension funds has followed that same advice when I’ve given it to them. Instead, these investors politely thank me for my thoughts and depart to listen to the siren song of a high-fee manager or, in the case of many institutions, to seek out another breed of hyper-helper called a consultant.

In defense of the bet, Seides wrote:

Having the flexibility to invest both long and short, hedge funds do not set out to beat the market. Rather, they seek to generate positive returns over time regardless of the market environment. They think very differently than do traditional “relative-return” investors, whose primary goal is to beat the market, even when that only means losing less than the market when it falls. For hedge funds, success can mean outperforming the market in lean times, while underperforming in the best of times. Through a cycle, nevertheless, top hedge fund managers have surpassed market returns net of all fees, while assuming less risk as well. We believe such results will continue.

So Buffett invested in a Vanguard index fund and Seides picked five hedge funds of funds. On December 31, 2017, the outcome was clear: the S&P 500 had trounced the hedge funds and Buffett won his bet.

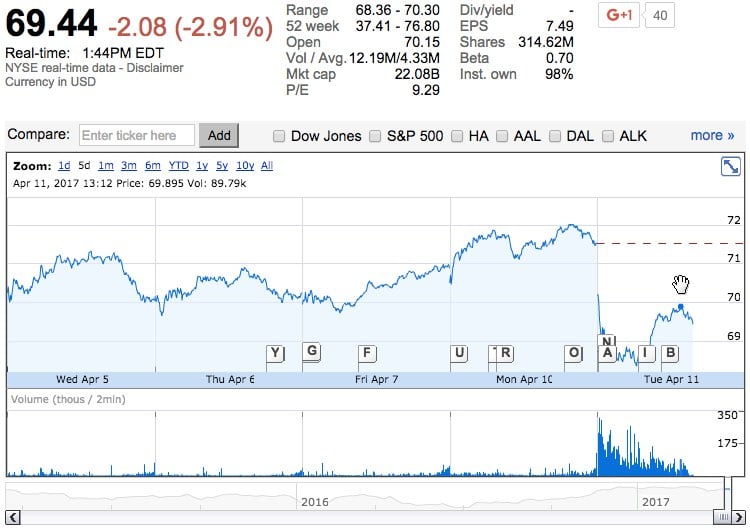

Yesterday, a video of a man dragged from an overbooked United flight because he wouldn’t give up his seat went viral. Public reaction to the incident and United’s subsequent fumbling of the aftermath has resulted in UAL’s stock falling several percentage points this morning:

The stock has rebounded slightly this afternoon and will probably fully recover within the next few weeks.

Update: It took about three and a half weeks, but on May 2, United’s stock had regained all of the value “lost” due to the incident and subsequent PR blunders. As of this writing (May 3 at 12:41 PM ET), UAL is actually up about 3.5% from the closing price before the incident.

In the most recent video from Marginal Revolution University, Tyler Cowen explains how the role of financial intermediaries contributed to the financial crisis of 2008. He highlights homeowners and banks taking on too much leverage, poorly planned incentive systems, securitization of mortgages, and banks making loans that are over-reliant on investor confidence.

By 2008, the economy was in a very fragile state, with both homeowners and banks taking on greater leverage, many ending up “underwater.” Why did managers at financial institutions take on greater and greater risk? We’ll discuss a couple of key reasons, including the role of excess confidence and incentives.

In addition to homeowners’ leverage and bank leverage, a third factor played a major role in tipping the scale toward crisis: securitization. Mortgage securities during this time were very hard to value, riskier than advertised, and filled to the brim with high risk loans. Cowen discusses several reasons this happened, including downright fraud, failure of credit rating agencies, and overconfidence in the American housing market.

Finally, a fourth factor joins homeowners’ leverage, bank leverage, and securitization to inch the economy closer to the edge: the shadow banking system. On the whole, the shadow banking system is made up of investment banks and various other complex financial intermediaries, highly dependent on short term loans.

When housing prices started to fall in 2007, it was the final nudge that pushed the economy over the cliff. There was a run on the shadow banking system. Financial intermediaries came crashing down. We faced a credit crunch, and many businesses stopped growing. Layoffs ensued, increasing unemployment.

On Last Week Tonight last night, John Oliver not only blasted the debt buying industry but ended up starting a company, bought $15 million worth of medical debt from Texas, and forgave it.

Update: I forgot to add, Occupy Wall Street did a similar thing back in 2012.

OWS is going to start buying distressed debt (medical bills, student loans, etc.) in order to forgive it. As a test run, we spent $500, which bought $14,000 of distressed debt. We then ERASED THAT DEBT. (If you’re a debt broker, once you own someone’s debt you can do whatever you want with it - traditionally, you hound debtors to their grave trying to collect. We’re playing a different game. A MORE AWESOME GAME.)

At the last minute Wilson told us LWT did not want to associate themselves with the work of the Rolling Jubilee due to its roots in Occupy Wall Street. Instead John Oliver framed the debt buy as his idea: a giveaway to compete with Oprah. The lead researcher who worked on this segment invoked the cover of journalism to justify distancing themselves from our project.

A huge cache of data has leaked from a Panama-based tax firm that shows how some of the world’s politicians and the rich hide their money in offshore tax havens. The video above, from the Guardian, is a quick 1:30 introduction on how these offshore havens work.

The documents show the myriad ways in which the rich can exploit secretive offshore tax regimes. Twelve national leaders are among 143 politicians, their families and close associates from around the world known to have been using offshore tax havens.

A $2bn trail leads all the way to Vladimir Putin. The Russian president’s best friend — a cellist called Sergei Roldugin — is at the centre of a scheme in which money from Russian state banks is hidden offshore. Some of it ends up in a ski resort where in 2013 Putin’s daughter Katerina got married.

Among national leaders with offshore wealth are Nawaz Sharif, Pakistan’s prime minister; Ayad Allawi, ex-interim prime minister and former vice-president of Iraq; Petro Poroshenko, president of Ukraine; Alaa Mubarak, son of Egypt’s former president; and the prime minister of Iceland, Sigmundur Davíð Gunnlaugsson.

Here is an important bit:

Are all people who use offshore structures crooks?

No. Using offshore structures is entirely legal. There are many legitimate reasons for doing so. Business people in countries such as Russia and Ukraine typically put their assets offshore to defend them from “raids” by criminals, and to get around hard currency restrictions. Others use offshore for reasons of inheritance and estate planning.

Are some people who use offshore structures crooks?

Yes. In a speech last year in Singapore, David Cameron said “the corrupt, criminals and money launderers” take advantage of anonymous company structures. The government is trying to do something about this. It wants to set up a central register that will reveal the beneficial owners of offshore companies. From June, UK companies will have to reveal their “significant” owners for the first time.

Update: The Panama Papers have claimed their first political victim. The now-former prime minister of Iceland has resigned because of his family’s offshore investments.

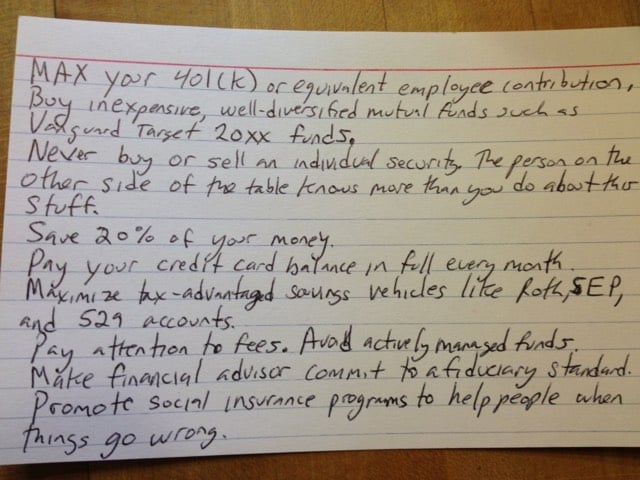

The Index Card is a new book by Helaine Olen and Harold Pollack about simple advice for personal finance. The idea for the book came about when Pollack jotted down financial advice that works for almost everyone on a 4x6 index card.

Now, Pollack teams up with Olen to explain why the ten simple rules of the index card outperform more complicated financial strategies. Inside is an easy-to-follow action plan that works in good times and bad, giving you the tools, knowledge, and confidence to seize control of your financial life.

But there’s a powerful truth here, which is that people dispensing financial advice are even less neutral than we realise. We’re good at spotting the obvious conflicts of interest: of course mortgage providers always think it’s a great time to buy a house; of course the sharp-suited guys from SpeedyMoola.co.uk think their payday loans are good value. But it’s more difficult to see that everyone offering advice has a deeper vested interest: they need you to believe things are complex enough to make their assistance worthwhile. It’s hard to make a living as a financial adviser by handing clients an index card and telling them never to return; and those stock-tipping columns in newspapers would be dull if all they ever said was “ignore stock tips”. Yes, the world of finance is complex, but it doesn’t follow that you need a complex strategy to navigate it.

There’s no reason to assume this situation only occurs with money, either. The human body is another staggeringly complex system, but based on current science, Michael Pollan’s seven-word guidance — “Eat food, not too much, mostly plants” — is probably wiser than all other diets.

In fact, most American slaves were not kidnapped on another continent. Though over 12.7 million Africans were forced onto ships to the Western hemisphere, estimates only have 400,000-500,000 landing in present-day America. How then to account for the four million black slaves who were tilling fields in 1860? “The South,” the Sublettes write, “did not only produce tobacco, rice, sugar, and cotton as commodities for sale; it produced people.” Slavers called slave-breeding “natural increase,” but there was nothing natural about producing slaves; it took scientific management. Thomas Jefferson bragged to George Washington that the birth of black children was increasing Virginia’s capital stock by four percent annually.

Here is how the American slave-breeding industry worked, according to the Sublettes: Some states (most importantly Virginia) produced slaves as their main domestic crop. The price of slaves was anchored by industry in other states that consumed slaves in the production of rice and sugar, and constant territorial expansion. As long as the slave power continued to grow, breeders could literally bank on future demand and increasing prices. That made slaves not just a commodity, but the closest thing to money that white breeders had. It’s hard to quantify just how valuable people were as commodities, but the Sublettes try to convey it: By a conservative estimate, in 1860 the total value of American slaves was $4 billion, far more than the gold and silver then circulating nationally ($228.3 million, “most of it in the North,” the authors add), total currency ($435.4 million), and even the value of the South’s total farmland ($1.92 billion). Slaves were, to slavers, worth more than everything else they could imagine combined.

Virginia slaveowners won a major victory when Thomas Jefferson’s 1808 prohibition of the African slave trade protected the domestic slave markets for slave-breeding.

I haven’t read the book, but I imagine they touched on the fact that by growing slave populations, southern states were literally manufacturing more political representation due to the Three-Fifths clause in the US Constitution. They bred more slaves to help politically safeguard the practice of slavery.

In the 1830s, powerful Southern slaveowners wanted to import capital into their states so they could buy more slaves. They came up with a new, two-part idea: mortgaging slaves; and then turning the mortgages into bonds that could be marketed all over the world.

First, American planters organized new banks, usually in new states like Mississippi and Louisiana. Drawing up lists of slaves for collateral, the planters then mortgaged them to the banks they had created, enabling themselves to buy additional slaves to expand cotton production. To provide capital for those loans, the banks sold bonds to investors from around the globe — London, New York, Amsterdam, Paris. The bond buyers, many of whom lived in countries where slavery was illegal, didn’t own individual slaves — just bonds backed by their value. Planters’ mortgage payments paid the interest and the principle on these bond payments. Enslaved human beings had been, in modern financial lingo, “securitized.”

Slave-backed securities. My stomach is turning again. (via @daveg)

2. President James Polk speculated in slaves, based on inside information he obtained from being President and shaping policy toward slaves and slave importation.

3. In the South there were slave “breeding farms,” where the number of women and children far outnumbered the number of men.

As historian Edward Baptist reveals in The Half Has Never Been Told, slavery and its expansion were central to the evolution and modernization of our nation in the 18th and 19th centuries, catapulting the US into a modern, industrial and capitalist economy. In the span of a single lifetime, the South grew from a narrow coastal strip of worn-out tobacco plantations to a sub-continental cotton empire. By 1861 it had five times as many slaves as it had during the Revolution, and was producing two billion pounds of cotton a year. It was through slavery and slavery alone that the United States achieved a virtual monopoly on the production of cotton, the key raw material of the Industrial Revolution, and was transformed into a global power rivaled only by England.

Cities, businesses, and artists are producing small batches of paper currency designed to be spent locally. I love the £20 note from Bristol, England (above)…it’s got Wallace’s head on it!

The local currency, though, is intended not as collectible but to encourage trade at the community businesses where they are accepted, rather than chain stores, where money taken in tends to flow out of town and into the coffers of multinational corporations. (Compare it to the farmers’ market: Homegrown lettuce now has a whole new meaning.)

“If you use a local currency, you keep the money local, and that has a ‘lifts all boats’ vibe to it,” said David Wolman, the author of “The End of Money.”

This metaphorical explanation of the post-2008 Irish banking crisis works equally well as an explanation for contemporary global financial markets in general.

Mary is the proprietor of a bar in Dublin. She realises that virtually all of her customers are unemployed alcoholics and, as such, can no longer afford to patronise her bar — she will go broke.

To solve this problem, she comes up with a new marketing plan that allows her customers to drink now, but pay later.

She keeps track of the drinks consumed on a ledger (thereby granting the customers loans).

Word gets around about Mary’s ‘drink now, pay later’ marketing strategy and, as a result, increasing numbers of customers flood into Mary’s bar.

Soon she has the largest sales volume for any bar in Dublin — all is starting to look rosy.

By providing her customers freedom from immediate payment demands Mary gets no resistance when, at regular intervals, she substantially increases her prices for wine and beer, the most consumed beverages.

A young and dynamic vice-president at the local bank recognises that these customer debts constitute valuable future assets and increases Mary’s borrowing limit.

He sees no reason for any undue concern, since he has the debts of the unemployed alcoholics as collateral.

At the bank’s corporate headquarters, expert traders figure a way to make huge commissions, and transform these customer loans into Drinkbonds and Alkibonds. These securities are then bundled and traded on international security markets.

The new investors don’t really understand that the securities being sold to them as ‘AAA’ secured bonds are really the debts of unemployed alcoholics. They have had a ‘rating house’ certify they are of good quality.

In 1997, Max-Hervé George’s father bought a unique policy from a French insurance company that functions like Grays Sports Almanac from Back to the Future II, only for financial markets. The policy allows George to invest in investment funds offered by the insurance company at prices up to a week old, essentially traveling back in time with knowledge of which investments will increase in price the most.

For instance, he might have his money in an Aviva fund invested in the French stock market. Lets say the Nikkei 225 rises 5 per cent during the week. He’ll tell Aviva to move his investments into its Japanese fund, at the price before the market moved.

At last report, in 2007, George’s investments were worth €1.4 million and growing at a rate of 68.6% per year. Assuming that rate holds and he continues investing his entire allocation optimally, George will be a billionaire in five years, would be able to buy the insurance company in question by 2025, and be worth a whopping €234 billion by 2030.

2. No person under the age of 35 will be allowed to work on Wall Street.

Upon leaving school, young people, no matter how persuasively dimwitted, will be required to earn their living in the so-called real economy. Any job will do: fracker, street performer, chief of marketing for a medical marijuana dispensary. If and when Americans turn 35, and still wish to work in finance, they will carry with them memories of ordinary market forces, and perhaps be grateful to our society for having created an industry that is not subjected to them. At the very least, they will know that some huge number of people — their former fellow street performers, say — will be seriously pissed off at them if they do risky things on Wall Street to undermine the real economy. No one wants a bunch of pissed-off street performers coming after them.

At that level, Shake Shack would debut at 50 times projected earnings of about $20 million this year, the people said, asking not to be named because the details are private. The company has tapped JPMorgan Chase & Co. and Morgan Stanley to manage the share sale, said the people.

That valuation would put it in line with other dining chains that have tapped into investor appetite for new stocks in recent years. El Pollo Loco Holdings Inc. (LOCO), which raised $123 million in July, now trades at about 60 times projected 2014 earnings, while Potbelly (PBPB) Corp. trades at over 64 times estimated earnings, data compiled by Bloomberg show.

Shake Shack is a modern day “roadside” burger stand serving a classic American menu of premium burgers, hot dogs, crinkle-cut fries, shakes, frozen custard, beer and wine. Founded by Danny Meyer’s Union Square Hospitality Group, LLC (“USHG”), Shake Shack was created leveraging USHG’s expertise in community building, hospitality, fine dining, restaurant operations and sourcing premium ingredients. Danny’s vision of Enlightened Hospitality guided the creation of the unique Shake Shack culture that, we believe, creates a differentiated experience for our guests across all demographics at each of the 63 Shacks around the world. As Shake Shack’s Board Chairman and USHG’s Chief Executive Officer, Danny has drawn from USHG’s experience creating and operating some of New York City’s most acclaimed and popular restaurants, including Union Square Cafe, Gramercy Tavern, Blue Smoke, The Modern, Maialino and Marta, to build what we believe is a new fine casual restaurant category in Shake Shack.

There are now 63 Shake Shacks. 63! I just wish the one across from the office would reopen. (via @caseyjohnston)

A simple theory of IPOs suggests that they arrive when a product or company is experiencing “peak buzz,” or at least when the insiders in the privately held company think they are at or near peak buzz. This will maximize the expected returns on the IPO when it comes to market.

When it comes to food, peak buzz usually arrives a wee bit after peak quality, given reputational lags. So if you are seeing peak buzz, it is probably time to bail on the restaurant, at least on a restaurant which is going to be sold. Bailing on the restaurant may in fact be slightly overdue.

To test Cowen’s theory1, I went to the Shake Shack in Grand Central today (12/31/14). I stood in line for 10 minutes, ordered my customary Shack burger with fries (long live the crinkle cut), and then waited an additional 10 minutes for my food. Verdict: as delicious as ever. Service was snappy and friendly. Well worth the wait and price for me: I got exactly what I wanted.

This is BS actually. I’ve been jonesing for a Shack burger for weeks now and I finally made it happen today.↩

I’ve learned that short-term thinking is at the root of most of our problems, whether it’s in business, politics, investing, or work.

I’ve learned that debt can cause more social problems than some drugs, yet drugs are illegal and debt is tax deductible.

I’ve learned that finance is actually very simple, but it’s made to look complicated to justify fees.

Unfortunately, the list is undermined almost completely by the get-rich-quick advertising on the site, including this bit at the end of the article, which I can’t even tell is an ad or just a promotion:

Opportunities to get wealthy from a single investment don’t come around often, but they do exist, and our chief technology officer believes he’s found one. In this free report, Jeremy Phillips shares the single company that he believes could transform not only your portfolio, but your entire life. To learn the identity of this stock for free and see why Jeremy is putting more than $100,000 of his own money into it, all you have to do is click here now.

Short-term thinking is at the root of most of our problems, click here now. Now!

A new study finds that insider trading is much worse than commonly thought: a quarter of all public company deals may involve some kind of insider trading. From the NY Times:

The professors examined stock option movements — when an investor buys an option to acquire a stock in the future at a set price — as a way of determining whether unusual activity took place in the 30 days before a deal’s announcement.

The results are persuasive and disturbing, suggesting that law enforcement is woefully behind — or perhaps is so overwhelmed that it simply looks for the most egregious examples of insider trading, or for prominent targets who can attract headlines.

The professors are so confident in their findings of pervasive insider trading that they determined statistically that the odds of the trading “arising out of chance” were “about three in a trillion.” (It’s easier, in other words, to hit the lottery.)

Only about 5% of the deals are ever litigated by the SEC. (via mr)

Mike Merrill reimagines the game of Monopoly to better represent the modern financial system by adding the banker as a player, convertible notes, and Series A financing.

Each player starts with only $500. That’s a nice bit of cash, but it’s going to be expensive to build your capitalist empire. Baltic Avenue will cost you $80, States Avenue is $140, Atlantic is $260, and that leaves you just $20. Even if you’re the first to land on Boardwalk you won’t be able to afford the $400 price tag. Another $200 from “passing Go” is not going to last that long. You need more money.

At the start of the game the banker will offer each player a convertible note of $1000 at a 20% discount and 5% interest*. Armed with $1500 the player is now ready to set out on their titan of the universe adventure! (Of course players are not required to take the convertible note.)

Michael Lewis’s new book about high-frequency trading dropped on Monday with less than 24 hours notice and the media is scrambling to catch up. There’s plenty of love for Lewis and his books out there, but Tyler Cowen has been linking to some critiques. For Bloomberg, Matt Levine writes:

In my alternative Michael Lewis story, the smart young whippersnappers build high-frequency trading firms that undercut big banks’ gut-instinct-driven market making with tighter spreads and cheaper trading costs. Big HFTs like Knight/Getco and Virtu trade vast volumes of stock while still taking in much less money than the traditional market makers: $688 million and $623 million in 2013 market-making revenue, respectively, for Knight and Virtu, versus $2.6 billion in equities revenue for Goldman Sachs and $4.8 billion for J.P. Morgan. Even RBC made 594 million Canadian dollars trading equities last year. The high-frequency traders make money more consistently than the old-school traders, but they also make less of it.

1. HFT doesn’t prey on small mom-and-pop investors. In his first two TV appearances, Lewis stuck to a simple pitch: Speed traders have rigged the stock market, and the biggest losers are average, middle-class retail investors-exactly the kind of people who watch 60 Minutes and the Today show. It’s “the guy sitting at his ETrade account,” Lewis told Matt Lauer. The way Lewis sees it, speed traders prey on retail investors by “trading against people who don’t know the market.”

The idea that retail investors are losing out to sophisticated speed traders is an old claim in the debate over HFT, and it’s pretty much been discredited. Speed traders aren’t competing against the ETrade guy, they’re competing with each other to fill the ETrade guy’s order.

This vagueness about time is one of the weaknesses of the book: it’s hard to keep track of time, and a lot of it seems to be an exposé not of high-frequency trading as it exists today, but rather of high-frequency trading as it existed during its brief heyday circa 2008. Lewis takes pains to tell us what happened to the number of trades per day between 2006 and 2009, for instance, but doesn’t feel the need to mention what has happened since then. (It is falling, quite dramatically.) The scale of the HFT problem - and the amount of money being made by the HFT industry - is in sharp decline: there was big money to be made once upon a time, but nowadays it’s not really there anymore. Because that fact doesn’t fit Lewis’s narrative, however, I doubt I’m going to find it anywhere in his book.

Flash Boys is about a small group of Wall Street guys who figure out that the U.S. stock market has been rigged for the benefit of insiders and that, post-financial crisis, the markets have become not more free but less, and more controlled by the big Wall Street banks. Working at different firms, they come to this realization separately; but after they discover one another, the flash boys band together and set out to reform the financial markets. This they do by creating an exchange in which high-frequency trading-source of the most intractable problems-will have no advantage whatsoever.

The characters in Flash Boys are fabulous, each completely different from what you think of when you think “Wall Street guy.” Several have walked away from jobs in the financial sector that paid them millions of dollars a year. From their new vantage point they investigate the big banks, the world’s stock exchanges, and high-frequency trading firms as they have never been investigated, and expose the many strange new ways that Wall Street generates profits.

His latest target, high-frequency trading, comprises a diverse set of software-driven strategies that have spread from U.S. equity markets to most developed countries as computer power grew and regulators tried to break the grip of centralized exchanges. While the tactics vary, they usually employ super-fast computers to post and cancel orders at rates measured in thousandths or even millionths of a second to capture price discrepancies on more than 50 public and private venues that make up the American equities market.

I don’t know too much about it but from what I’ve read, high-frequency trading seems to involve huge Wall Street banks using the Office Space/Richard-Pryor-in-Superman-III trick of shaving fractions of a penny off of trillions of trades every year, except that it’s perfectly legal. The NY Times has an excerpt of the book to further whet your appetite.

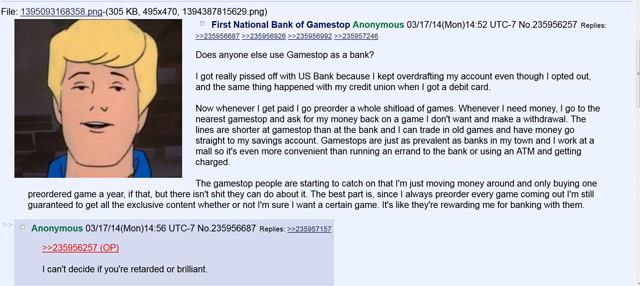

An anonymous user of 4chan has come up with a brilliantly harebrained scheme for their personal banking. They use video game retailer GameStop as a bank.

Here’s how it works: whenever a paycheck comes in, this person goes to GameStop and pre-orders a bunch of upcoming video games. Whenever they need money, they go to the GameStop and cancel a game or two to make a withdrawal. Here’s the entire scheme:

Does anyone else use Gamestop as a bank?

I got really pissed off with US Bank because I kept overdrafting my account even though I opted out, and the same thing happened with my credit union when I got a debit card.

Now whenever I get paid I go preorder a whole shitload of games. Whenever I need money, I go to the nearest gamestop and ask for my money back on a game I don’t want and make a withdrawal. The lines are shorter at gamestop than at the bank and I can trade in old games and have money go straight to my savings account. Gamestops are just as prevalent as banks in my town and I work at a mall so it’s even more convenient than running an errand to the bank or using an ATM and getting charged.

The gamestop people are starting to catch on that I’m just moving money around and only buying one preordered game a year, if that, but there isn’t shit they can do about it. The best part is, since I always preorder every game coming out I’m still guaranteed to get all the exclusive content whether or not I’m sure I want a certain game. It’s like they’re rewarding me for banking with them.

I love the bits about the trade-ins and the rewards. (via @caseyjohnston)

Stay Connected