This week, the Bureau of Labor Statistics released its latest estimate for the share labor receives of national income for the first quarter of 2024. The statistics shows the income workers receive compared with the productivity their labor generates.

According to BLS, this income share has declined for non-farm workers from about two-thirds, 64.1% in the first quarter of 2001, to 55.8% in the first quarter of 2024.

Roughly speaking, in the first quarter of 2024, workers received ~56% of the income generated by their labor and 44% went to capital (ownership & shareholders).

Here’s a graph that shows the labor share of national income from 1947 to 2016 so you can get some idea of the decline that’s happened:

Scene on Radio hosts John Biewen and Ellen McGirt described labor share of national income like so:

Ellen McGirt: The labor share of national income. So, of all the income that businesses bring in, from sales of their goods and services, how much of that goes to workers. As opposed to, how much winds up as profits in the pockets of stockholders.

John Biewen: That number, according to the Federal Reserve, also went up significantly during the “thirty glorious years” in the United States. In the before times, in 1930, workers took home about 57% of the money that was generated by their labor. 57%. That labor share went up in the 1940s, to about 65% — almost two-thirds of corporate income was going to workers. It stayed over 60% for the next few decades, well into the 1970s.

Ellen McGirt: That doesn’t sound like a huge increase — from fifty-some percent to sixty-some percent. But the result, over those decades, was trillions of dollars in the pockets of people in the bottom 90-percent of the income scale — that’s money that would have gone to the wealthiest folks without those more progressive policies that reduced inequality. And then, guess what, starting in about 1975, the labor share of national income went down, and down. Until now, things are more like they were back in the days of Herbert Hoover.

This observation by McGirt is important but kind of hard to follow in text so I’ll restate it: when you’re talking about something as massive as the US economy, even a difference of a few percentage points in the labor share of national income over several years is trillions and trillions of dollars. And increasingly, those trillions are going to the wealthiest and not to the bottom 90%.

According to a groundbreaking new working paper by Carter C. Price and Kathryn Edwards of the RAND Corporation, had the more equitable income distributions of the three decades following World War II (1945 through 1974) merely held steady, the aggregate annual income of Americans earning below the 90th percentile would have been $2.5 trillion higher in the year 2018 alone. That is an amount equal to nearly 12 percent of GDP — enough to more than double median income — enough to pay every single working American in the bottom nine deciles an additional $1,144 a month. Every month. Every single year.

Price and Edwards calculate that the cumulative tab for our four-decade-long experiment in radical inequality had grown to over $47 trillion from 1975 through 2018. At a recent pace of about $2.5 trillion a year, that number we estimate crossed the $50 trillion mark by early 2020. That’s $50 trillion that would have gone into the paychecks of working Americans had inequality held constant — $50 trillion that would have built a far larger and more prosperous economy — $50 trillion that would have enabled the vast majority of Americans to enter this pandemic far more healthy, resilient, and financially secure.

Marlene Engelhorn inherited millions from her family and decided to give much of it away (€25 million). She formed an independent council called Guter Rat für Rückverteilung (“good council for redistribution”) made up of 50 randomly selected Austrians chosen to reflect the makeup of Austria’s population, and they decided where to direct the money. Engelhorn’s mission statement is worth a read:

Democracy is about cultivating relationships: a society works on doing well. And a society is doing well when the people in that society are doing well. At the moment, this does not apply to everyone: wealth, assets and property are distributed unequally and unfairly. And so is the power in our society.

In Austria, the richest one percent of the population hoards up to 50 percent of the net wealth. This means that one hundredth of society owns just under half of the wealth. And 99 percent of people have to make do with the other half. Almost four million households struggle to get by every day. And the one percent? Most of them have simply inherited.

We are talking about dynasties that amass wealth and power over generations. They then withdraw from our society as if it were none of their business. I also come from such a dynasty. My wealth was accumulated before I was even born. It was accumulated because other people did the work, but my family was able to inherit the ownership of an enterprise and thus all claims to the fruits of its labour.

Wealth is never an individual achievement. Wealth is always created by society. A few people get rich because they buy other people’s time and profit from it. Because they have a patent on a product that others urgently need. Because they buy a piece of land that increases in value and because society builds infrastructure around it. In the process, they destroy the environment to harvest the resources.

I enjoyed this roast of how we handle money in America by The Daily Show’s Ronny Chieng.

He goes after income & sales taxes:

America decided filing taxes should be as quick and painless as getting a root canal at the DMV. You got your 1099s, your Form 1040, your Schedule C, your R2-D2, your Blink-182. You spend days trying to figure out what you owe the government and then the government tells you if are you right because apparently they knew the whole frigging time. It is like the world’s most pointless game show.

Tipping:

Everywhere else, a tip is a show of appreciation, not a GoFundMe for someone who doesn’t earn a living wage. A waiter’s ability to pay rent shouldn’t be dependent on how generous Becky feels after three martinis.

And our currency:

In other countries, every denomination is a different size because it makes it easier to tell them apart, especially if you are blind. But apparently blind people don’t need to use money in America ‘cause look at this shit. Same exact size, all of it. You gotta look over each individual bill to figure out which slaveowner to hand over.

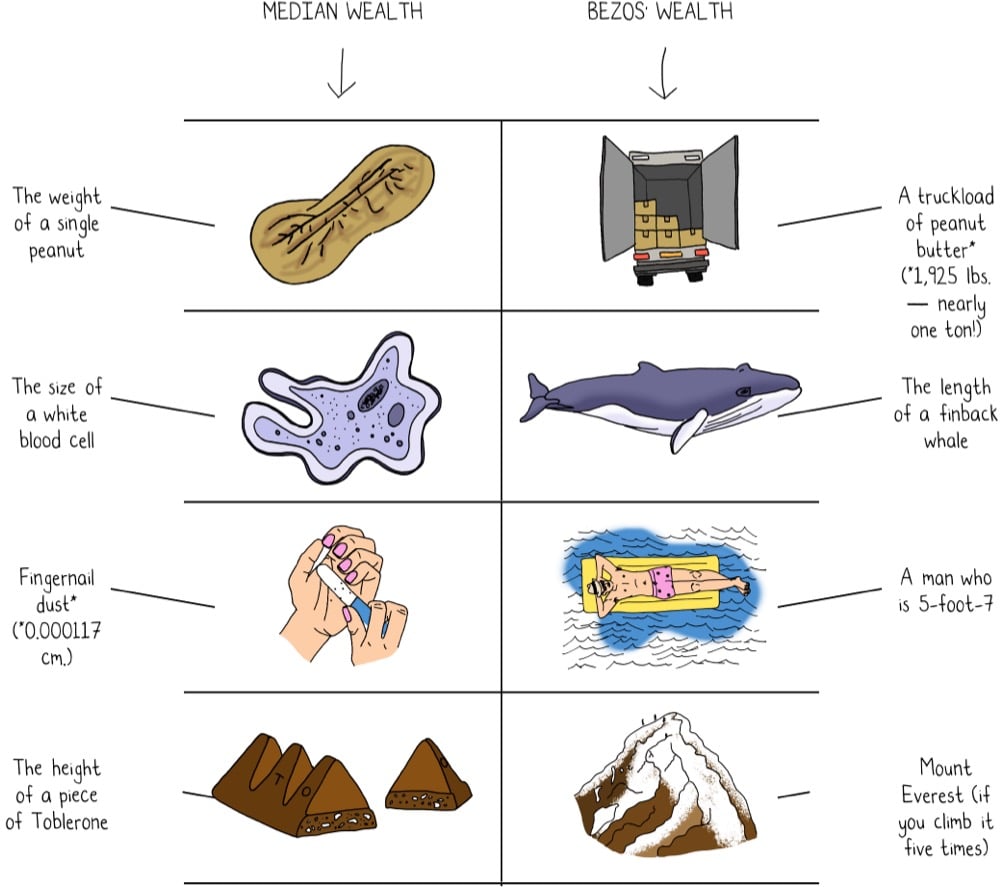

In 9 Ways to Imagine Jeff Bezos’ Wealth, Mona Chalabi provides us with some data visualizations that can help us wrap our heads around just how much money Amazon founder Jeff Bezos has. For instance, if the width of an Oreo cookie represents the median net worth of a US household, Bezos’ wealth is twice the width of the Grand Canyon.

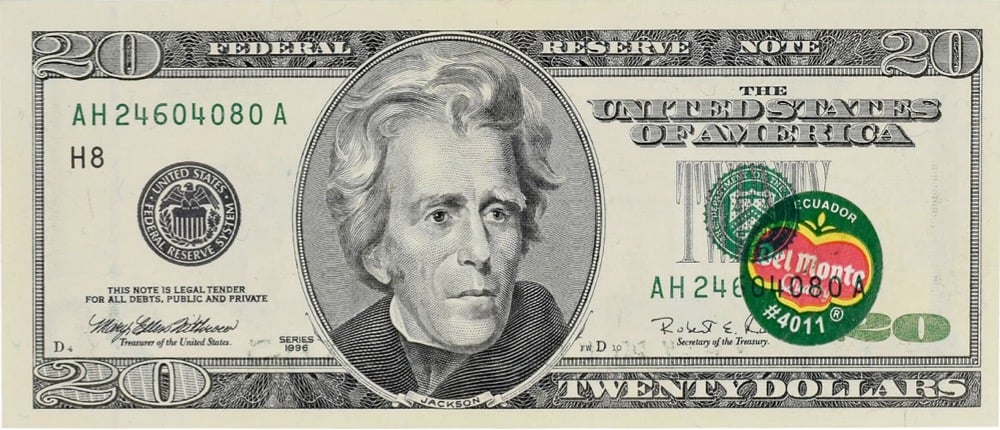

Somehow, during the printing process at a US Treasury Department printing facility, this $20 bill got a Del Monte banana sticker affixed to it…and then the seal and serial number was printed over it. The bill, known as the Del Monte Note, was sold at auction in January 2021 for $396,000.

The Western response has been far broader than most experts anticipated, and threatens to throw the Russian economy into chaos. Yet there’s a catch. Absent significant domestic reforms in the West — reforms that should have been enacted long ago — sanctions targeted at the oligarchic and official figures close to Russian President Vladmir Putin risk inflicting little more than a flesh wound on Russia’s imperial kleptocracy.

Rampant financial anonymity in places like the U.S. makes it relatively easy for powerful rich people to evade sanctions. A Russian oligarch may have multimillion-dollar mansions in Washington, D.C.; or multiple steel plants across the Rust Belt; or a controlling stake in a hedge fund in Greenwich, Connecticut; or an entire fleet of private jets in California; or an array of lawyers setting up purchases at art houses around the country. And all of that wealth can be hidden-perfectly legally-behind anonymous shell companies and trusts that are enormously difficult to penetrate.

If Western policy makers hope to hold Putin’s cronies truly accountable, sanctions will have to be paired with pro-transparency reforms that can disassemble this web of secrecy. Western governments should start by ending anonymity in shell companies and trusts; demanding basic anti-money-laundering checks for lawyers, art gallerists, and auction-house managers; and closing loopholes that allow anonymity in the real-estate, private-equity, and hedge-fund industries. That is, if the sanctions are to retain their bite, the entire counter-kleptocracy playbook needs to be implemented-immediately.

In this entertaining and informative video, Oliver Bullough, who has written a pair of books on money laundering (Moneyland and the forthcoming Butler to the World) takes us on a tour of London while telling us how “the most efficient scaled-up money laundering system in the world” has helped Russia’s oligarchs hide their billions and keep Putin in power. Bullough also wrote about the UK’s role in laundering oligarch money recently in The Guardian.

Russia is a mafia state, and its elite exists to enrich itself. Democracy is an existential threat to that theft, which is why Putin has crushed it at home and seeks to undermine it abroad. For decades, London has been the most important place not only for Russia’s criminal elite to launder its money, but also for it to stash its wealth. We have been the Kremlin’s bankers, and provided its elite with the financial skills it lacks. Its kleptocracy could not exist without our assistance. The best time to do something about this was 30 years ago — but the second best time is right now.

We journalists have long been writing about this, but it is not simply overheated rhetoric from overexcited hacks. Parliament’s intelligence and security committee wrote two years ago that our investigative agencies are underfunded, our economy is awash with dirty money, and oligarchs have bought influence at the very top of our society.

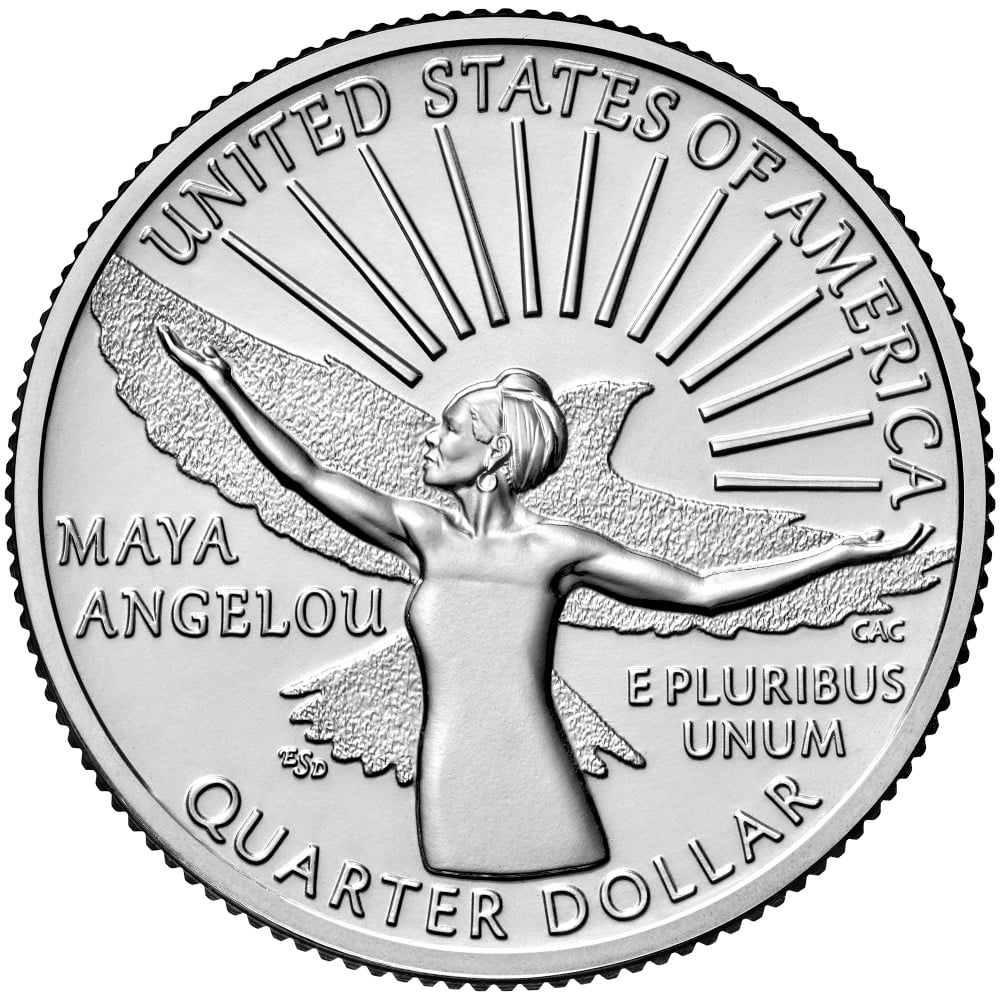

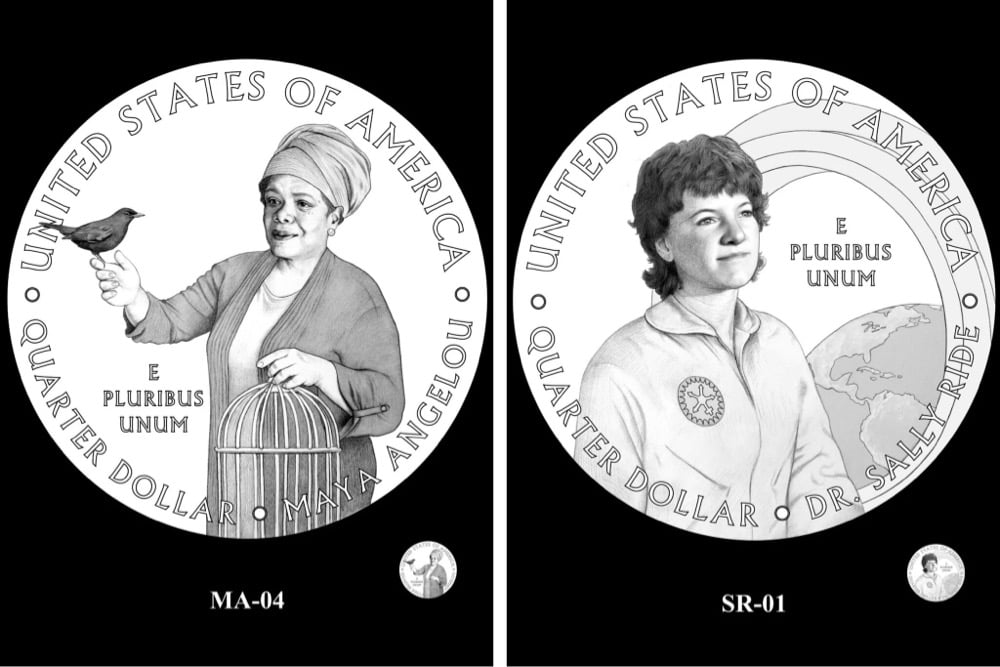

A writer, poet, performer, social activist, and teacher, Angelou rose to international prominence as an author after the publication of her groundbreaking autobiography, “I Know Why the Caged Bird Sings.” Angelou’s published works of verse, non-fiction, and fiction include more than 30 bestselling titles. Her remarkable career encompasses dance, theater, journalism, and social activism.

The front of the Angelou quarter features a portrait of George Washington (a slaveowner, I feel it is important to note) that is different from the usual image on regular quarters. The new image was sculpted by Laura Gardin Fraser in 1931:

In 1931, Congress held a competition to design a coin to honor the 200th anniversary of George Washington’s birth. The original competition called for the obverse of the coin to feature a portrait of George Washington, based on the famed life-mask bust by French sculptor Jean-Antoine Houdon. The reverse was to feature a design that was to be “national” in nature.

Laura Gardin Fraser submitted a design that features a right-facing portrait of George Washington on the obverse, while the reverse shows an eagle with wings spread wide. In a 1932 letter to recommend Fraser’s design, the U.S. Commission of Fine Arts (CFA) wrote to (then) Treasury Secretary Andrew W. Mellon:

“This bust is regarded by artists who have studied it as the most authentic likeness of Washington. Such was the skill of the artist in making this life-mask that it embodies those high qualities of the man’s character which have given him a place among the great of the world…Simplicity, directness, and nobility characterize it. The design has style and elegance…The Commission believes that this design would present to the people of this country the Washington whom they revere.”

While her design was popular, it was not chosen. Instead, Secretary Mellon ultimately selected the left-facing John Flannigan design, which has appeared on the quarter’s obverse since 1932.

Beginning in 2022 and continuing through 2025, the Mint will issue five quarters in each of these years. The ethnically, racially, and geographically diverse group of individuals honored through this program reflects a wide range of accomplishments and fields, including suffrage, civil rights, abolition, government, humanities, science, space, and the arts. The additional honorees in 2022 are physicist and first woman astronaut Dr. Sally Ride; Wilma Mankiller, the first female principal chief of the Cherokee Nation and an activist for Native American and women’s rights; Nina Otero-Warren, a leader in New Mexico’s suffrage movement and the first female superintendent of Santa Fe public schools; and Anna May Wong, the first Chinese American film star in Hollywood, who achieved international success despite racism and discrimination.

The Angelou quarter will start circulating later this month and early next month — look for it in your change soon!

Starting in 2022, the US Mint will release into circulation 20 quarters featuring notable American women as part of the American Women Quarters Program. From the US Mint:

The American Women Quarters may feature contributions from a variety of fields, including, but not limited to, suffrage, civil rights, abolition, government, humanities, science, space, and the arts. The women honored will be from ethnically, racially, and geographically diverse backgrounds. The Public Law requires that no living person be featured in the coin designs.

Topic asked more than a dozen people how they spent sudden windfalls of money. Among those queried were two MacArthur grant winners, people who inherited money, game show winners, a professional poker player, and a woman who lost her house because of Hurricane Maria. TV writer & editor Danielle Henderson:

The only directive I’ve ever given my agent, my manager, anyone on my team, is to make sure I get paid like a white man. I do not want to get any offers that are lower than average because I’m a woman or I’m black. I’m not out here demanding a quadrillion dollars, but if I see that somebody’s sold a project for a certain amount and my project is in a similar vein, I’m not settling for less than that.

Planetary scientist Sara Seager:

When I got my MacArthur award in 2013, they asked, “What are you going to spend the money on?” I said, “I’m going to spend it all on household help so I can spend more time with my kids and more time on my job.”

If you have kids, or a person who relies solely on you, not only do you have to take care of them and want to spend time with them, but you have to make their breakfast and their lunch, if they’re really little. And then clean up after them. There’s this endless series of chores. I got tons of responses from people saying, “I can’t believe you said that,” because people won’t admit that. People don’t want to admit the price you pay for working.

A big check, for $70,000. No, we’re not talking a big Publishers Clearing House grand-prize check, but it was definitely the biggest check I’d ever held with my name on it.

I gazed at the statement, then closed my eyes for a moment and said to myself:

“I can build mom a home now.”

It was the first time I felt truly successful in every sense of the word.

Nick Hiller has rebooted his great-great-grandfather’s textiles & dry goods store (established in Detroit in 1904) as an online shop. The first collection is called the Currency Blankets Collection, and features lovely blankets inspired by patterns on banknotes from around the world.

For thousands of years, textiles were so basic to survival that they functioned as a form of currency. In Mesoamerica, the Zapotecs paid tribute in woven rugs to the ruling Aztecs; in North America, the Navajos transacted in Pendleton blankets with European settlers; in West Africa, the Wolof in Gambia used “cloth money” in standardized strips that could be torn to make change; in medieval Iceland, a woolen fabric called wadmal (Old Norse for “legal cloth”) was the official currency for over 600 years. Even the Silk Road, civilization’s first global trade network, was named after the route’s dominant form of currency.

The blankets in the collection are manufactured in the US and reflect banknotes from France, the US (the pattern is a super zoom of Ben Franklin’s cheek on the $100 bill), Romania, Sierra Leone, Switzerland, Argentina, and several others.

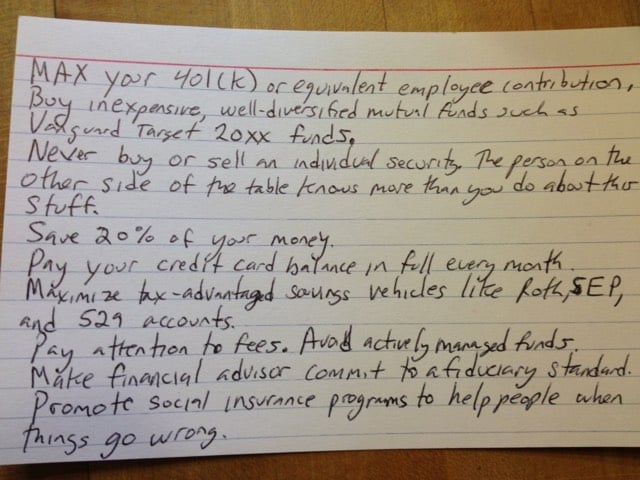

The Index Card is a new book by Helaine Olen and Harold Pollack about simple advice for personal finance. The idea for the book came about when Pollack jotted down financial advice that works for almost everyone on a 4x6 index card.

Now, Pollack teams up with Olen to explain why the ten simple rules of the index card outperform more complicated financial strategies. Inside is an easy-to-follow action plan that works in good times and bad, giving you the tools, knowledge, and confidence to seize control of your financial life.

But there’s a powerful truth here, which is that people dispensing financial advice are even less neutral than we realise. We’re good at spotting the obvious conflicts of interest: of course mortgage providers always think it’s a great time to buy a house; of course the sharp-suited guys from SpeedyMoola.co.uk think their payday loans are good value. But it’s more difficult to see that everyone offering advice has a deeper vested interest: they need you to believe things are complex enough to make their assistance worthwhile. It’s hard to make a living as a financial adviser by handing clients an index card and telling them never to return; and those stock-tipping columns in newspapers would be dull if all they ever said was “ignore stock tips”. Yes, the world of finance is complex, but it doesn’t follow that you need a complex strategy to navigate it.

There’s no reason to assume this situation only occurs with money, either. The human body is another staggeringly complex system, but based on current science, Michael Pollan’s seven-word guidance — “Eat food, not too much, mostly plants” — is probably wiser than all other diets.

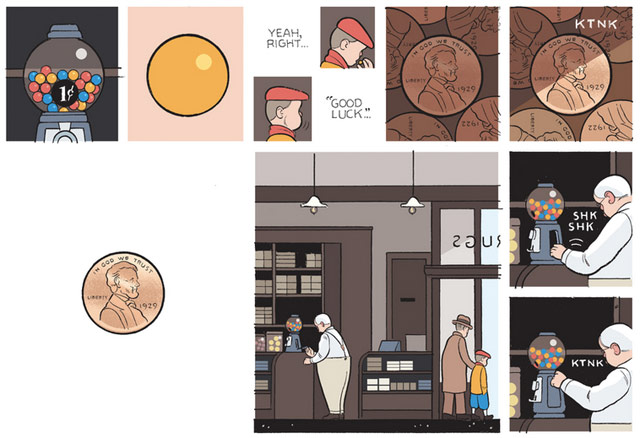

This week on Last Week Tonight, John Oliver rails against the penny. This seems like such an obvious thing, that we should stop using pennies, but I bet if the government ever moved to ban pennies, it would set off a firestorm of protest.

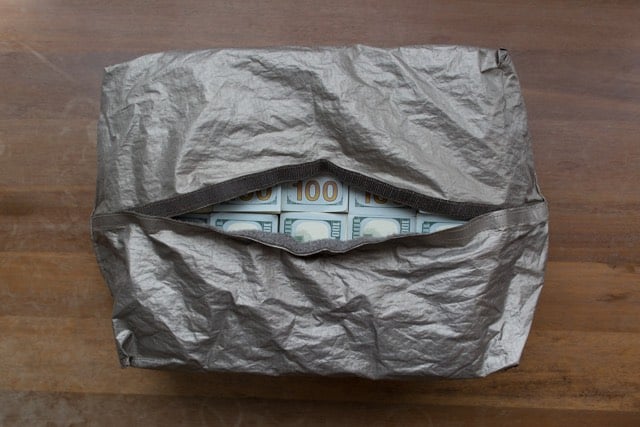

A site called SDR Traveller sells ultralight, strong, and discreet bags for traveling to places where such things are necessary. Their most eye-catching item is the 1M Hauly Heist, a bag designed to carry US$1 million in cash that also doubles as a Faraday cage for shielding your electronics from radio frequency tracking.

From the description on the page for the 1M Hauly (which holds the million bucks without the RF shielding):

In many countries project expenses and payroll for the local crew need to be carried in cash. Whether you’re managing a team of thirty working for months at the edge of the grid, or on a solo trip to negotiate a significant cash transaction, the 1M Hauly is designed for discreet, safe carry of up to $1 Million USD in strapped, new or used $100 USD banknotes.

Designed to address the six main issues with carrying significant volume banknotes in field: risk of discovery; risk of damage (especially in high-humidity, monsoon environments); container robustness; carryability; glide; and in-field accounting.

Note that $1 million in $100 bills weights 20.4lbs. The site also sells smaller money pouches (in $10k, $100k, and $400k carrying capacities) as well as a durable duffel. All the bags are made from Cuben Fiber, a material originally used for yacht sails that’s four times stronger than Kevlar at only half the weight. (via @craigmod)

Four years into a twenty-year study of the mental conditions of kids living in rural North Carolina, a quarter of the participants experienced a dramatic increase in annual income. The researchers used this opportunity to find out how that increase in wealth affected the wellbeing of the kids. What they learned is that even a little money goes a long way.

Not only did the extra income appear to lower the instance of behavioral and emotional disorders among the children, but, perhaps even more important, it also boosted two key personality traits that tend to go hand in hand with long-term positive life outcomes.

The first is conscientiousness. People who lack it tend to lie, break rules and have trouble paying attention. The second is agreeableness, which leads to a comfort around people and aptness for teamwork. And both are strongly correlated with various forms of later life success and happiness.

Cities, businesses, and artists are producing small batches of paper currency designed to be spent locally. I love the £20 note from Bristol, England (above)…it’s got Wallace’s head on it!

The local currency, though, is intended not as collectible but to encourage trade at the community businesses where they are accepted, rather than chain stores, where money taken in tends to flow out of town and into the coffers of multinational corporations. (Compare it to the farmers’ market: Homegrown lettuce now has a whole new meaning.)

“If you use a local currency, you keep the money local, and that has a ‘lifts all boats’ vibe to it,” said David Wolman, the author of “The End of Money.”

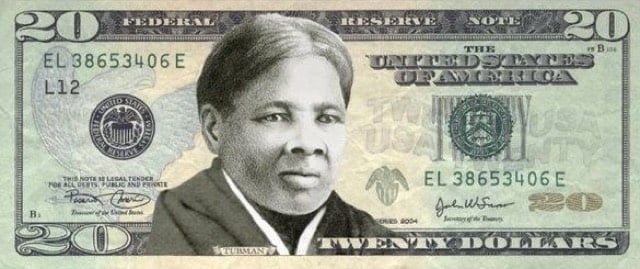

Adding her voice to a chorus of others, Amy Davidson makes a great case for putting Harriet Tubman on the US $20 bill and kicking Andrew Jackson to the curb.

On September 17, 1849, Araminta, who now called herself Harriet, ran away to freedom, along with two of her brothers. Their owner, Eliza Brodess-Pattison’s granddaughter-in-law-had been making moves to sell them, and the fear was that the family would be broken up. Brodess put an ad in the local newspaper, offering a hundred-dollar reward each for “Minty,” Harry, and Ben. (The only extant copy of the ad was found in 2003, in a dumpster.) Almost immediately, Tubman began making trips back to Maryland, organizing the escapes of relatives, friends, and scores of other slaves, often just ahead of armed men pursuing them. On one trip, she discovered that her husband, John Tubman, who was free himself, was living with another woman; he had no interest in going north. He is a man who seems not to have known Tubman’s worth.

When I was a kid, I read a lot of biographies1 on people like Ben Franklin, Thomas Edison, Abraham Lincoln, and the Wright brothers. My favorite, which I read at least three times, was Ann Petry’s Harriet Tubman: Conductor on the Underground Railroad. Tubman is one of history’s greatest badasses. Put her on the damn bill.

Our local public library had a series of biographies for kids…I wish I could remember what these books were. I did a little research just now but nothing came up. I remember them being small (hardcovers but the size of paperbacks), no dust jackets, and plainly titled (e.g. “Abraham Lincoln”). There were around 50 titles and must have been 20-30 years old when I read them in the early 80s. I devoured them as a kid and would love to pass them along to my kids.↩

Roger Pasquier hunts for coins on NYC sidewalks and keeps track of how much he finds. He discovered an odd consequence of everyone having a smartphone: people don’t pick up change on the sidewalk anymore.

From 1987 to 2006, he averaged about fifty-eight dollars a year. Then Apple introduced the iPhone, and millions of potential competitors started to stare at their screens rather than at the sidewalks. Since 2007, Pasquier has averaged just over ninety-five dollars a year.

I know, I know, that’s anecdotal and correlation != causation and whatever, but that’s an interesting theory.

For her master’s project, Barbara Bernát designed a set of fictional banknotes: the Hungarian Euro.

I am a total sucker for banknote mockups and aside from the simplicity, what caught my eye about Bernát’s project is the one security feature: if you look at the notes under a UV light, you see the skeletons of the animals depicted on the notes:

Mobile devices and software advances have helped to create a burgeoning on-demand economy that — in some places — makes it possible to live your life without leaving your house (and if you do decide to leave, it’s easy to order a car). But that’s only part of the story. In Quartz, Leo Mirani explains how he experienced the on-demand economy long before tech revolution:

These luxuries are not new. I took advantage of them long before Uber became a verb, before the world saw the first iPhone in 2007, even before the first submarine fibre-optic cable landed on our shores in 1997. In my hometown of Mumbai, we have had many of these conveniences for at least as long as we have had landlines — and some even earlier than that. It did not take technology to spur the on-demand economy. It took masses of poor people.

The SHA-256 algorithm is surprisingly simple, easy enough to do by hand. (The elliptic curve algorithm for signing Bitcoin transactions would be very painful to do by hand since it has lots of multiplication of 32-byte integers.) Doing one round of SHA-256 by hand took me 16 minutes, 45 seconds. At this rate, hashing a full Bitcoin block (128 rounds) would take 1.49 days, for a hash rate of 0.67 hashes per day (although I would probably get faster with practice). In comparison, current Bitcoin mining hardware does several terahashes per second, about a quintillion times faster than my manual hashing. Needless to say, manual Bitcoin mining is not at all practical.

I don’t have any awesome ideas for how to invest a buck, unfortunately. That is my weakness. My first instinct was to invest it in a stripper’s g-string or a barista’s tip jar. But I’m not sure how that translates as investment. I do know that the more frequently you visit/tip a barista — your neighborhood barista, who does not work at a Starbucks — the more often you are treated like family and you get free coffee. I think that the more you invest in a stripper, the less you get free things from that stripper.

One way or another, Bitcoin is going to be huge. It could be the as big as the Internet, it could transform into something else, or it could be one of tech’s biggest busts. Meanwhile, many of us are still wondering exactly what it is (it’s both a currency and means of transporting that currency). GQ’s Marshall Sella decided to score some of this newfangled dough and “blow it on all the pleasures that Bitcoin can buy.” Sex, Drugs, and Toasters: My Life on Bitcoin.

Within two months, I’d be visiting Charlie Shrem at his parents’ place, where he was wearing an ankle monitor and living under house arrest.

(That sounds like the beginning of every great startup story.)

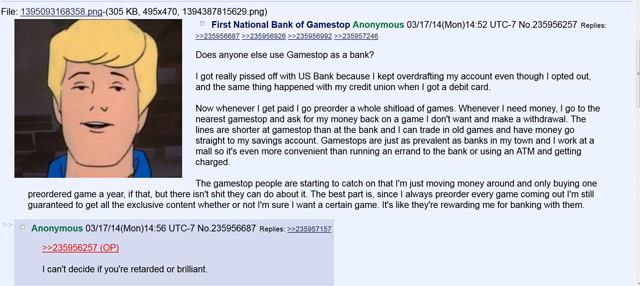

An anonymous user of 4chan has come up with a brilliantly harebrained scheme for their personal banking. They use video game retailer GameStop as a bank.

Here’s how it works: whenever a paycheck comes in, this person goes to GameStop and pre-orders a bunch of upcoming video games. Whenever they need money, they go to the GameStop and cancel a game or two to make a withdrawal. Here’s the entire scheme:

Does anyone else use Gamestop as a bank?

I got really pissed off with US Bank because I kept overdrafting my account even though I opted out, and the same thing happened with my credit union when I got a debit card.

Now whenever I get paid I go preorder a whole shitload of games. Whenever I need money, I go to the nearest gamestop and ask for my money back on a game I don’t want and make a withdrawal. The lines are shorter at gamestop than at the bank and I can trade in old games and have money go straight to my savings account. Gamestops are just as prevalent as banks in my town and I work at a mall so it’s even more convenient than running an errand to the bank or using an ATM and getting charged.

The gamestop people are starting to catch on that I’m just moving money around and only buying one preordered game a year, if that, but there isn’t shit they can do about it. The best part is, since I always preorder every game coming out I’m still guaranteed to get all the exclusive content whether or not I’m sure I want a certain game. It’s like they’re rewarding me for banking with them.

I love the bits about the trade-ins and the rewards. (via @caseyjohnston)

People had assumed that the name of the secretive creator of Bitcoin, Satoshi Nakamoto, was a pseudonym designed to protect his anonymity. Newsweek’s Leah McGrath Goodman tracked down a man who could be the Bitcoin founder and discovered that his real name is…Satoshi Nakamoto.

Two police officers from the Temple City, Calif., sheriff’s department flank him, looking puzzled. “So, what is it you want to ask this man about?” one of them asks me. “He thinks if he talks to you he’s going to get into trouble.”

“I don’t think he’s in any trouble,” I say. “I would like to ask him about Bitcoin. This man is Satoshi Nakamoto.”

“What?” The police officer balks. “This is the guy who created Bitcoin? It looks like he’s living a pretty humble life.”

I’d come here to try to find out more about Nakamoto and his humble life. It seemed ludicrous that the man credited with inventing Bitcoin - the world’s most wildly successful digital currency, with transactions of nearly $500 million a day at its peak - would retreat to Los Angeles’s San Bernardino foothills, hole up in the family home and leave his estimated $400 million of Bitcoin riches untouched. It seemed similarly implausible that Nakamoto’s first response to my knocking at his door would be to call the cops. Now face to face, with two police officers as witnesses, Nakamoto’s responses to my questions about Bitcoin were careful but revealing.

Tacitly acknowledging his role in the Bitcoin project, he looks down, staring at the pavement and categorically refuses to answer questions.

“I am no longer involved in that and I cannot discuss it,” he says, dismissing all further queries with a swat of his left hand. “It’s been turned over to other people. They are in charge of it now. I no longer have any connection.”

Nice bit of sleuthing by Goodman. But given the interest around Bitcoin, it’s amazing that it took this long, even with Nakamoto’s first name change.

Update: The subject of Newsweek’s story now denies he was the creator of Bitcoin.

Rest is a luxury for the rich. I get up at 6AM, go to school (I have a full courseload, but I only have to go to two in-person classes) then work, then I get the kids, then I pick up my husband, then I have half an hour to change and go to Job 2. I get home from that at around 1230AM, then I have the rest of my classes and work to tend to. I’m in bed by 3. This isn’t every day, I have two days off a week from each of my obligations. I use that time to clean the house and soothe Mr. Martini and see the kids for longer than an hour and catch up on schoolwork. Those nights I’m in bed by midnight, but if I go to bed too early I won’t be able to stay up the other nights because I’ll fuck my pattern up, and I drive an hour home from Job 2 so I can’t afford to be sleepy. I never get a day off from work unless I am fairly sick. It doesn’t leave you much room to think about what you are doing, only to attend to the next thing and the next. Planning isn’t in the mix.

Her response to the first (agressively negative) comment is worth reading as well.

But here’s the trick: if you can’t buy happiness by spending more money on higher quality, then you can buy happiness by spending money taking advantage of all the reasons why people still engage in blind tastings, despite the fact that they are a very bad way to judge a wine’s quality. If you know what the wine you’re tasting is, if you know where it comes from, if you know who made it, if you’ve met the winemaker, and in general, if you know how expensive it is — then that knowledge deeply affects — nearly always to the upside — the way in which you taste and appreciate the wine in question.

Stay Connected